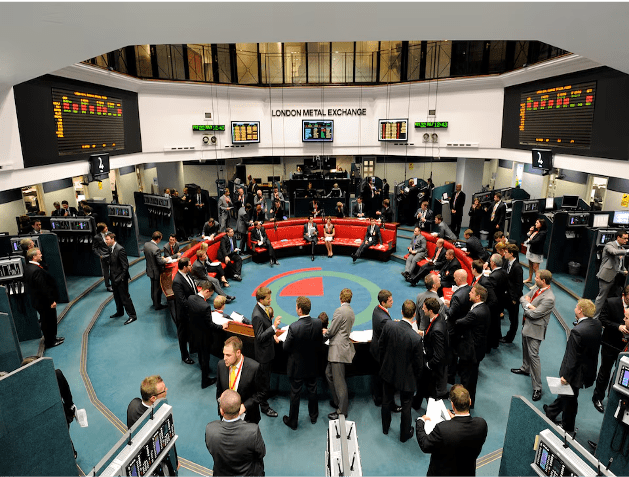

Hedge fund Elliott challenges court verdict it lost against LME on nickel

LONDON, July 9 (Reuters) - U.S.-based hedge fund Elliott Associates on Tuesday urged a London court to overturn a verdict supporting the London Metal Exchange's (LME) cancellation of nickel trades partly because the exchange failed to disclose documents. The LME annulled $12 billion in nickel trades in March 2022 when prices shot to records above $100,000 a metric ton in a few hours of chaotic trade. Elliott and market maker Jane Street Global Trading brought a case demanding a combined $472 million in compensation, alleging at a trial in June last year that the 146-year-old exchange had acted unlawfully. London's High Court ruled last November that the LME had the right to cancel the trades because of exceptional circumstances, and was not obligated to consult market players prior to its decision. Lawyers for Elliott told London's Court of Appeal that the LME belatedly released documents in May detailing its "Kill Switch" and "Trade Halt" internal procedures. It also newly disclosed an internal report that Elliott said detailed potential conflicts of interest at the exchange. "It was troubling that one gets disclosure out of the blue in the Court of Appeal for the first time," Elliott lawyer Monica Carss-Frisk told the court. Jane Street Global did not appeal the ruling. "If we had had them (documents) in the proceedings before the divisional court, we may well have sought permission to cross examine." LME lawyers said the new documents were not relevant. "The disclosed documents do not affect the reasoning of the divisional court or the merits of the arguments on appeal," the exchange said in documents prepared for the appeal hearing. "Elliott's appeal is largely a repetition of the arguments which were advanced, and rightly rejected." The LME said it had both the power and a duty to unwind the trades because a record $20 billion in margin calls could have led to at least seven clearing members defaulting, systemic risk and a potential "death spiral". Elliott said the ruling diluted protection provided by the Human Rights Act and also wrongly concluded the LME had the power to cancel the trades.

NASA plays 'blame-shifting' game with China as lunar soil research set to start

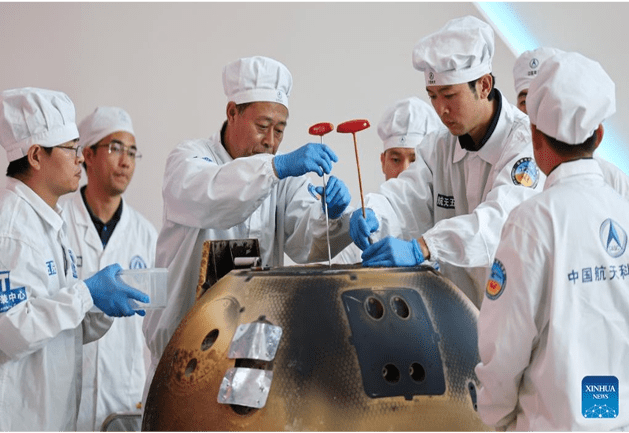

The returner of the Chang'e-6 lunar probe is opened during a ceremony at the China Academy of Space Technology under the China Aerospace Science and Technology Corporation in Beijing, capital of China, June 26, 2024. The returner of the Chang'e-6 lunar probe was opened at a ceremony in Beijing on Wednesday afternoon. During the ceremony at the China Academy of Space Technology under the China Aerospace Science and Technology Corporation, researchers opened the returner and examined key technical indicators. Photo: Xinhua As the US space industry recently faced yet more delays and stagnation with key components including manned spacecraft and space suits "going wrong," NASA has once again resorted to its "sour grapes" rhetoric upon seeing China's successful retrieval of fresh lunar soils from the far side of the moon, by claiming that China did not directly invite its scientists to participate in the lunar soil research. This behavior is a typical blame-shifting trick, Chinese experts said, noting it is clear to all that it is the US' own laws, not China, that are restricting space cooperation between the two sides. Instead of deceiving themselves by distorting the truth, the US should face up to its own problem of overall weakening engineering capability and the lack of long-term planning in its space industry. After the Chang'e-6 samples, weighing nearly 2 kilograms, were safely transported to a special laboratory for further study on Friday, NASA spokesperson Faith McKie told media that while China worked with the European Space Agency, France, Italy and Pakistan on this mission, "NASA wasn't invited to take part in the moon probe." NASA also didn't get "any direct invitation" to study China's moon rocks, after it welcomed all scientists from around the world to apply to study them, McKie told NatSec Daily. Responding to the remarks, Chinese Foreign Ministry spokesperson Mao Ning told the Global Times on Monday that China is open to having space exchanges with the US, and we also welcome countries around the world to take part in the study of lunar samples. "However, the US side seems to have forgotten to mention its domestic legislation such as the Wolf Amendment. The real question is whether US scientists and institutions are allowed by their own government to participate in cooperation with China," Mao said. "The existence of the Wolf Amendment has basically shut the door to space collaboration between the two countries," Wang Yanan, chief editor of Beijing-based Aerospace Knowledge magazine, told the Global Times on Monday. Even if research institutions of the US have the willingness to work with China on opportunities such as lunar sample research, institutions there must obtain special approval from the US Congress due to the presence of this amendment, Wang explained. Currently, no such "green light" is in sight from the Congress. Furthermore, China's collaboration with international partners is based on equality and mutual benefit, leveraging their respective scientific resources, facilities, and expertise. However, the US only wants what it doesn't have, and its engagement with China would be advantageous only to itself, Wang noted. NASA has found itself embroiled in a number of thorny issues recently, with the latest being Boeing's Starliner manned spaceship experiencing both helium leaks and thruster issues during a June 6 docking with the International Space Station (ISS), which led to an indefinite delay for its crew's return to Earth, despite NASA's insistence that they are not "stranded" in space. The return of the Starliner capsule, while has already been delayed by two weeks, will be put on hold "well into the summer" pending results of new thruster tests, which are scheduled to start Tuesday and will take approximately two weeks or even more, per NASA officials. Previously on June 24, NASA cancelled a spacewalk on the ISS following a "serious situation," when one of the spacesuits experienced coolant leak in the hatch. While being broadcast on a livestream, the astronauts reported "literally water everywhere" as they were preparing for the extravehicular activity, space.com reported. The report said that this is the second time this particular spacewalk was postponed, after a June 13 attempt with a different astronaut group was pushed back due to a "spacesuit discomfort." The recurring issues with the spacesuits are due to their much-extended service lifespan, media reported, as the puffy white ones US astronauts currently wear were designed more than 40 years ago. Despite the pressing need to replace them, NASA announced recently that it is abandoning a plan to develop next-generation spacesuits, which had been committed to be delivered by 2026, CNN reported on Thursday. One of the root causes for such problems is that the US has developed many large technology conglomerates, which for a long time have benefited significantly from government orders and industry monopolies. Consequently, in many complex engineering fields, the level of attention given is greatly insufficient, Wang noted. It also reflected the US' lack of long-term strategic planning for its manned space program. For instance, the ageing spacesuits should have been replaced a decade ago to ensure that operational suits remain in usable condition. Failure to address this issue results in a hindrance to the space station's necessary maintenance tasks and even poses life-threatening risks to astronauts in emergency situations, experts said. The issues with Boeing's spacecraft and the spacesuits are not isolated problems, but reflected a systemic issue in the US space industry - the overall weakening of engineering capabilities, they noted.

The Apple Watch is reportedly getting a birthday makeover

Apple is planning to revamp its smartwatch as its 10th birthday nears. The improvements include larger displays and thinner builds, Bloomberg reported. The revamped watches may also get a new chip, which could enable some AI enhancements. The Apple Watch is about to turn 10, so Apple is planning a birthday revamp, including larger displays and thinner builds, Bloomberg reported. Both versions of the new Series 10 watches will have screens similar to the large displays found on the Apple Watch Ultra, the report said. The revamped watches are also expected to contain a new chip that may permit some AI enhancements later on. Last month, Apple pulled back the curtain on its generative-AI plans with Apple Intelligence. Advertisement It hopes the artificial-intelligence features will prove alluring enough to persuade consumers to buy new Apple products. The announcement has been generally well received by Wall Street. Dan Ives of Wedbush Securities wrote in a Monday note that the "iPhone 16 AI-driven upgrade could represent a golden upgrade cycle for Cupertino." "We believe AI technology being introduced into the Apple ecosystem will bring monetization opportunities on both the services as well as iPhone/hardware front and adds $30 to $40 per share," he added. Apple's stock closed on Friday at just over $226 a share, up 22% this year and valuing the company at $3.47 trillion. That puts it just behind Microsoft, which was worth $3.48 trillion at Friday's close. The tech giants have been vying for the title of the world's most valuable company in recent months — with the chipmaker Nvidia briefing claiming the crown last month. Apple also announced some software updates for the watch at its Worldwide Developers Conference last month. The latest version of the device's software, watchOS 11, emphasizes fitness and health, introducing tools that allow users to rate workouts and adjust effort ratings. WatchOS 11 will also use machine learning to curate the best photos for users' displays. Apple has previously used product birthdays to release new versions of devices. The iPhone X's release marked the 10th anniversary of the smartphone. However, it's not clear exactly when Apple plans to release the revamped watches, Bloomberg said. The company announced the Apple Watch in September 2014, with CEO Tim Cook calling it "the most personal product we've ever made." Apple did not immediately respond to a request for comment made outside normal working hours.

Google extends Linux kernel support to 4 years

According to AndroidAuthority, the Linux kernel used by Android devices is mostly derived from Google's Android Universal Kernel (ACK) branch, which is created from the Android mainline kernel branch when new LTS versions are released upstream. For example, when kernel version 6.6 is announced as the latest LTS release, an ACK branch for Android15-6.6 appears shortly after, with the "android15" in the name referring to the Android version of the kernel (in this case, Android 15). Google maintains its own set of LTS kernel branches for three main reasons. First, Google can integrate upstream features that have not yet been released into the ACK branch by backporting or picking, so as to meet the specific needs of Android. Second, Google can include some features that are being developed upstream in the ACK branch ahead of time, making it available for Android devices as early as possible. Finally, Google can add some vendor or original equipment manufacturer (OEM) features for other Android partners to use. Once created, Google continues to update the ACK branch to include not only bug fixes for Android specific code, but also to integrate the LTS merge content of the upstream kernel branch. For example, the Linux kernel vulnerability disclosed in the July 2024 Android security bulletin will be fixed through these updates. However, it is not easy to distinguish a bug fix from other bug fixes, as a patch that fixes a bug may also accidentally plug a security vulnerability that the submitter did not know about or chose not to disclose. Google does its best to recognize this, but it inevitably misses the mark, resulting in bug fixes for the upstream Linux kernel being released months before Android devices. As a result, Google has been urging Android vendors to regularly update the LTS kernel to avoid being caught off guard by unexpectedly disclosed security vulnerabilities. Clearly, the LTS version of the Linux kernel is critical to the security of Android devices, helping Google and vendors deal with known and unknown security vulnerabilities. The longer the support period, the more timely security updates Google and vendors can provide to devices.