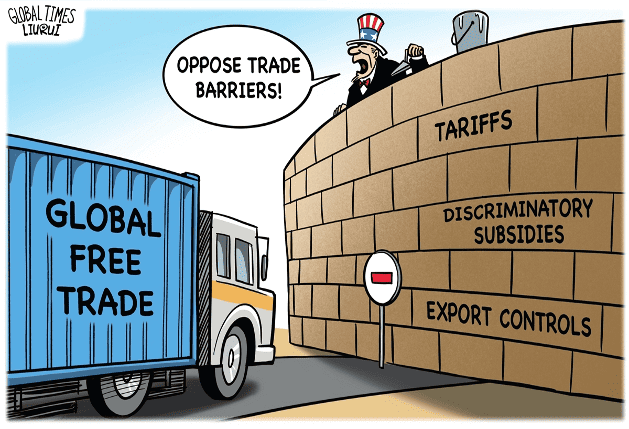

US politicians are advocating for steep tariffs, echoing the protectionist Fordney-McCumber Tariff of 1922. Despite potential international retaliation, risks to global economic rules and a shift from post-World War II principles, US politicians have promised to increase trade barriers against China, causing concerns for the sustainability of global economic harmony.

A century ago, the Republican Congress passed the Fordney-McCumber Tariff of 1922. This post-World War-I effort to protect the US from German competition and rescue America's own businesses from falling prices sparked a global wave of tariff hikes.

While long forgotten, echoes of Fordney-McCumber now reverberate across the US political landscape. Once again, politicians are grasping the tariff as a magic talisman against its own economic ills and to contain the rise of China.

The Democratic Party of the 1920s opposed tariffs, because duties are harmful to consumers and farmers, but today both President Joe Biden and former President Donald Trump favor national delivery through protectionism.

Trump promised that his second term, if elected, would impose 60-percent tariffs on everything arriving from China and 10-percent tariffs on imports from the rest of the world, apparently including the imports covered by 14 free trade agreements with America's 20 partners. He initially promised 100-percent tariffs on electric vehicles (EVs), but when Biden declared that he was hiking tariffs on EVs from China to 100-percent, Trump raised the ante to 200-percent.

On May 14, 2024, the White House imposed tariffs ranging from 25 percent (on items such as steel, aluminum and lithium batteries) to 50 percent (semiconductors, solar cells, syringes and needles) and 100 percent (electric vehicles) on Chinese imports. US government officials offer "national security" and "supply chain vulnerability" as the justification for levying high tariffs.

To deflect worries about inflation, US Trade Representative Katherine Tai declared, "first of all, I think that that link, in terms of tariffs to prices, has been largely debunked."

Contrary findings by the United States International Trade Commission and a number of distinguished economists, as well as Biden's own 2019 statement criticizing Trump's tariffs - "Trump doesn't get the basics. He thinks tariffs are being paid by China… [but] the American people are paying his tariffs" - forced Tai's office to wind back her declaration.

The fact that prohibitive barriers to imports of solar cells, batteries and EVs will delay the green economy carries zero political weight with Trump and little with Biden. Nor does either of them worry about the prospects of Chinese retaliation and damage to the fabric of global economic rules. Historical lessons - unanticipated consequences of the foolish Fordney-McCumber Tariff of 1922 and the Smoot-Hawley Tariff of 1930 - are seen as irrelevant by the candidates and their advisers.

The US' lurch from its post-World War II free trade principles offers China a golden opportunity. On the world stage, China will espouse open free trade and investment. China will encourage EV and battery firms to establish plants in Europe, Brazil, Mexico and elsewhere, essentially daring the US to damage its own alliances by restricting third country imports containing Chinese components.

Whether the fabric of global economic rules that has delivered astounding prosperity to the world will survive through the 21st century remains to be seen. Much will depend on the decisions of other large economic powers, not only China but also the European Union and Japan, as well as middle powers, such as Australia, Brazil, Chile, ASEAN and South Korea. Their actions and reactions will reshape the rules of the 21st century.

If others follow America down this costly path, the world will become less prosperous and vastly more unpredictable. If they resist, the US risks being diminished and more isolated.

The author is a non-resident Senior Fellow at the Peterson Institute of International Economics. bizopinion@globaltimes.com.cn