Sparkling box office for Spring Festival films indicates tremendous potential for movie consumption in Chinese society

According to Chinese movie ticketing platform Taopiaopiao, the box office for the 2024 Spring Festival holidays surpassed last year's 6.766 billion yuan and entered the top two in the history of Chinese Spring Festival holidays box office. I recently watched three movies, and I think they are all good. However, their overall level is not higher than the movies from last Spring Festival holidays. The higher box office compared to last year reflects the strong potential for movie consumption in Chinese society. Our filmmakers need to make further efforts. The current development of Chinese movies has many advantages. People often complain that our film creation faces various "restricted areas," but in terms of societal topics, the space for Chinese film creation is relatively large and relaxed. For example, Zhang Yimou's film Article 20 shows protest scenes and boldly explores the issue of judicial injustice in depth. A few years ago, the film I Am Not Madame Bovary specifically discussed the sensitive issue of petitioning. Another film, Johnny Keep Walking! which was aired last year, also touches on serious social issues. The breadth and depth of these films' topics lay the foundation for their attractiveness. The improvement of China's basic film production level has played a role in boosting their success, resulting in Hollywood films being collectively pushed off the Chinese box office charts. Now, almost any domestic film can be considered "watchable." The next step is to produce world-class masterpieces and promote the collective advancement of Chinese films on the global stage. The three movies that I watched are YOLO, directed, written and starring Jia Ling, a representative of the new generation of female Chinese directors, Pegasus 2, directed by Han Han and Article 20. They are all realistic-themed films, and the actors who play the main characters have some overlap. Although each of them is good, as mentioned earlier, I personally feel that their overall quality is not as good as films screened during last year's Spring Festival holidays. So I have a feeling that Chinese movies have been spinning in place for a year in such a good market environment. Of course, I am not an expert, so what I say may not be correct, or it may be biased. The production level of Chinese films, in terms of technology, has caught up. Domestic films have surpassed Hollywood in the domestic market through competition, which is a great achievement. However, I hope that this does not mark the beginning of a "decoupling" between Chinese movies and the rest of the world, but rather a turning point for Chinese films to reach a higher level domestically and to go global. This requires Chinese realistic films to not only be loved by domestic audiences but also become increasingly "understandable" to foreigners, allowing them to empathize with us through these films. If Chinese films can gradually go global through market-oriented approaches, it will be a new process for the international community to re-recognize and understand China, and to establish common values between us. The earliest understanding of the US by the Chinese people came entirely from the shaping of news propaganda. Later, American films and TV works entered China, showcasing the rich American society. Now, Western media's portrayal of China is completely stereotyped. If Chinese films and other popular culture do not go global, and if a large number of secular elements from China do not appear on the global internet, the outside world's perception of China is likely to be dictated by Western media for a long time. So I hope that China's excellent film market can incubate outstanding works that are loved and enjoyed globally. Not only should our cultural policies provide greater space, but our internet public opinion should also be more tolerant of the interweaving and mutually influencing between Chinese and Western cultural elements. We should not restrict those elements in Chinese films that can resonate with both Chinese and foreign audiences. For example, comedies should not only make Chinese people laugh, but also be understandable to foreigners. Chinese films need to establish their own big stars, including top-tier female stars. In the past, Bruce Lee and Jackie Chan became famous in the West, but they were primarily seen as "Hollywood stars." It is a more challenging journey for Chinese stars to gain international recognition through their own films. The success of Chinese films and Chinese stars worldwide is definitely a complementary process. The backgrounds of our film stories should also be carefully selected and more diverse, enhancing the visual quality and international appeal of the films. Feng Xiaogang's film Be There or Be Square was entirely set in the US, and later, there was another film called Lost in Thailand, both of which achieved good results. Choosing such backgrounds should be encouraged as one of the approaches. In conclusion, I am delighted by the comprehensive recovery of the Chinese film market, and I also hope that the films nurtured by this market will continue to progress. To achieve this, we need to keep introducing the world's best films and collaboratively cultivate the aesthetic taste of the Chinese people alongside Chinese films. Chinese films have already stood up, but they should not monopolize this vast market. Instead, the Chinese market should serve as the stage for them to expand globally.

How the iPhone 16 With AI Could Send Apple's Market Value to $4T

Apple could be on track to reach a $4 trillion market capitalization with the artificial intelligence (AI) iPhone 16 upgrade cycle coming, Wedbush analysts said. The analysts said the iPhone 16 supercharged with AI could bring a "golden upgrade cycle" for Apple. Apple's recently announced iOS 18 with Apple Intelligence and OpenAI partnership are also expected to create monetization opportunities and increase share value. Apple (AAPL) could be on the path to a $4 trillion market capitalization as an iPhone upgrade cycle approaches, driven by the iPhone 16 supercharged with artificial intelligence (AI) capabilities, according to Wedbush analysts. 1 Apple's recently announced iOS 18 with Apple Intelligence and OpenAI partnership are also expected to create monetization opportunities and increase share value. AI iPhone 16 Upgrade Cycle Coming Soon Wedbush analyst said that an AI iPhone 16 could bring "a golden upgrade cycle for Cupertino looking ahead with pent-up demand building globally." "The Street is now starting to slowly recognize that with Apple Intelligence on the doorstep in essence Cupertino will be the gatekeepers of the consumer AI Revolution," they said, with 2.2 billion iOS devices globally and 1.5 billion iPhones. Wedbush suggested a "consumer AI tidal wave" could start with the iPhone 16 in mid-September, adding that estimates indicate 270 million iPhones users have not upgraded in over four years. Recovery in China To Support Upgrade Cycle The analysts indicated that iPhone supply stabilization in Asia is also "a very good sign heading into a monumental iPhone 16 upgrade cycle." Wedbush's projections come amid ongoing concerns for the iPhone maker in the China region amid increased competition, though there have been recent signs of improving shipments. They projected that June "will be the last negative growth quarter for China with a growth turnaround beginning in the September quarter," when the iPhone 16 is expected to be released. AI and iOS 18 Could Also Boost Share Value Apple unveiled iOS 18 supercharged by Apple Intelligence and an AI partnership with OpenAI at its developers' conference in June. Wedbush analysts said the partnership with the Chat-GPT maker "creates the highway for developers around the globe to focus on iOS 18 and this in turn will create a myriad of monetization opportunities for Cook & Co. over the coming years." The analysts estimated that "this could result in incremental Services high margin growth annually of $10 billion for Apple" driven by hardware and software. They added they believe "AI technology being introduced into the Apple ecosystem will bring monetization opportunities on both the services as well as iPhone/hardware front and adds $30 to $40 per share." Apple shares were little changed in early trading Monday, though they have gained more than 17% since the start of the year. Do you have a news tip for Investopedia reporters? Please email us at tips@investopedia.com SPONSORED Trade on the Go. Anywhere, Anytime One of the world's largest crypto-asset exchanges is ready for you. Enjoy competitive fees and dedicated customer support while trading securely. You'll also have access to Binance tools that make it easier than ever to view your trade history, manage auto-investments, view price charts, and make conversions with zero fees. Make an account for free and join millions of traders and investors on the global crypto market.

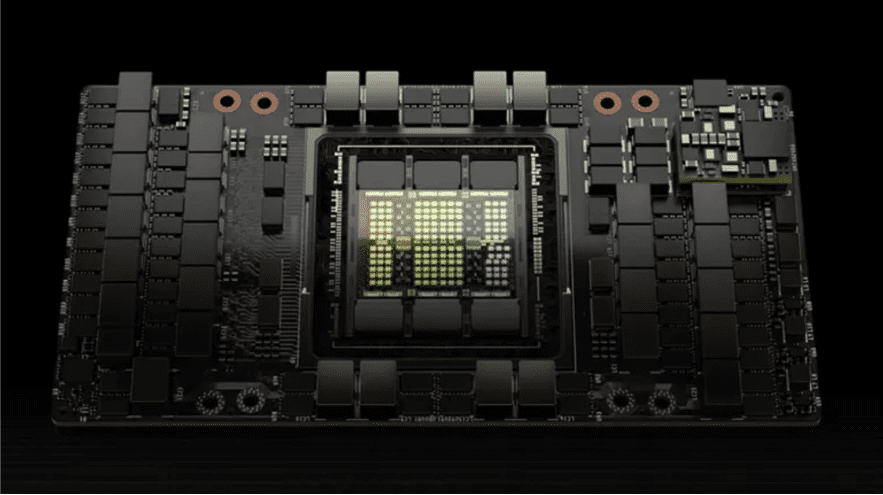

Nvidia H20 will sell 1 million units this year, contributing $12 billion in revenue!

Recently, according to the FT, citing the latest forecast data of the market research institute SemiAnalysis, AI chip giant NVIDIA will ship more than 1 million new NVIDIA H20 acceleration chips to the Chinese market this year, and it is expected that the cost of each chip is between $12,000 and $13,000. This is expected to generate more than $12 billion in revenue for Nvidia. Affected by the United States export control policy, Nvidia's advanced AI chip exports to China have been restricted, H20 is Nvidia based on H100 specifically for the Chinese market to launch the three "castration version" GPU among the strongest performance, but its AI performance is only less than 15% of H100, some performance is even less than the domestic Ascend 910B. When Nvidia launched the new H20 in the spring of this year, there were reports that due to the large castration of H20 performance, coupled with the high price, Chinese customers' interest in buying is insufficient, and they will turn more to choose China's domestic AI chips. Then there are rumors that Nvidia has lowered the price of the H20 in order to improve its competitiveness. However, the latest news shows that due to supply issues caused by the low yield of the Ascend 910B chip, Chinese manufacturers in the absence of supply and other better options, Nvidia H20 has started to attract new purchases from Chinese tech giants such as Baidu, Alibaba, Tencent and Bytedance. Analysts at both Morgan Stanley and SemiAnalysis said the H20 chip is now being shipped in bulk and is popular with Chinese customers, despite its performance degradation compared to chips Nvidia sells in the United States.

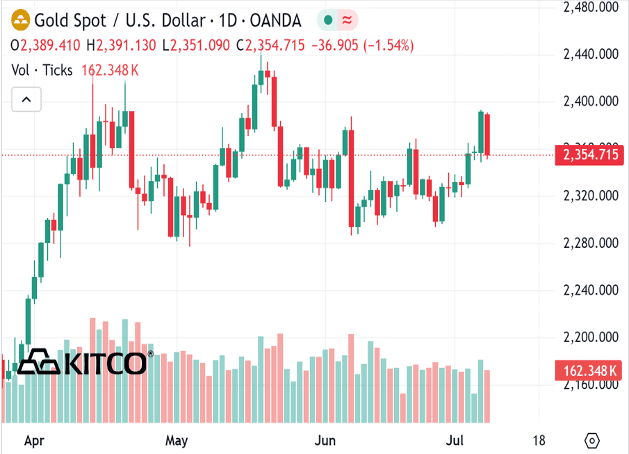

Gold, silver caught in downdraft of broad commodity market sell off

(Kitco News) - Gold and silver prices are sharply lower in midday U.S. trading Monday, on heavy profit-taking from the shorter-term futures traders after recent good price advances. The selling pressure today across most of the raw commodity spectrum is also keeping the precious metals bulls on the sidelines to start the trading week. August gold was last down $37.50 at $2,360.10. September silver was down $0.849 at $30.85. U.S. stock indexes mixed but near their record highs scored last week. The rallying stock market is a bearish element for the gold and silver markets, from a competing asset class perspective. The key U.S. data points of the week include Fed Chairman Powell’s speeches to the U.S. Congress on Tuesday and Wednesday, and the consumer and producer price indexes on Thursday and Friday, respectively. The key outside markets today see the U.S. dollar index slightly higher. Nymex crude oil prices are lower and trading around $82.25 a barrel. The benchmark 10-year U.S. Treasury note yield is presently 4.288%. Technically, August gold bulls have the overall near-term technical advantage. Bulls’ next upside price objective is to produce a close above solid resistance at the June high of $2,406.70. Bears' next near-term downside price objective is pushing futures prices below solid technical support at $2,300.00. First resistance is seen at $2,382.60 and then at $2,400070. First support is seen at $2,350.00 and then at last week’s low of $2,327.40. Wyckoff's Market Rating: 6.0. September silver futures bulls have the overall near-term technical advantage. Silver bulls' next upside price objective is closing prices above solid technical resistance at the May high of $33.05. The next downside price objective for the bears is closing prices below solid support at the June low of $28.90. First resistance is seen at $31.00 and then at $31.50. Next support is seen at Friday’s low of $30.45 and then at $30.00. Wyckoff's Market Rating: 6.5. (Hey! My “Markets Front Burner” weekly email report is my best writing and analysis, I think, because I get to look ahead at the marketplace and do some market price forecasting. Plus, I’ll throw in an educational feature to move you up the ladder of trading/investing success. And it’s free! Email me at jim@jimwyckoff.com and I’ll add your email address to my Front Burner list.)

Australia pledges to provide more funds to Pacific island banks to counter China's influence

Australia pledged on Tuesday to increase investment in Pacific island nations, offering A$6.3 million ($4.3 million) to support their financial systems. Some Western banks are cutting ties with the region because of risk factors, while China is trying to increase its influence there. Some Western bankers have terminated long-standing banking relationships with small Pacific nations, while others are considering closing operations and restricting access to dollar-denominated bank accounts in those countries. "We know that the Pacific is the fastest-moving region in the world for correspondent banking services," Australian Treasurer Jim Chalmers said in a speech at the Pacific Banking Forum in Brisbane. "What's at stake here is the Pacific's ability to engage with the world," he said, with much of the region at risk of being cut off from the global financial system. Chalmers said Australia would provide A$6.3 million ($4.3 million) to the Pacific to develop secure digital identity infrastructure and strengthen compliance with anti-money laundering and counter-terrorist financing requirements. Experts say Western banks are de-risking to meet financial regulations, making it harder for them to do business in Pacific island nations, where compliance standards sometimes lag, undermining their financial resilience. Australia's ANZ Bank is in talks with governments about how to make its Pacific island businesses more profitable amid concerns about rising Chinese influence as financial services leave the West, Chief Executive Shayne Elliott said Tuesday. ANZ is the largest bank in the Pacific region, with operations in nine countries, though some of those businesses are not financially sustainable, Elliott said in an interview on the sidelines of the forum. "If we were there purely for commercial purposes, we would have closed it a long time ago," he said. Western countries, which have traditionally dominated the Pacific, are increasingly concerned about China's plans to expand its influence in the region after it signed several major defense, trade and financial agreements with the region. Bank of China signed an agreement with Nauru this year to explore opportunities in the country, following Australia's Bendigo Bank saying it would withdraw from the country. Mr. Chalmers said Australia was working with Nauru to ensure that banking services in the country could continue. ANZ Bank exited its retail business in Papua New Guinea in recent years, while Westpac considered selling its operations in Fiji and Papua New Guinea but decided to keep them. The Pacific lost about 80% of its correspondent banking relationships for dollar-denominated services between 2011 and 2022, Australian Assistant Treasurer Stephen Jones told the forum, which was co-hosted by Australia and the United States. “We would be very concerned if there were countries acting in the region whose primary objective was to advance their own national interests rather than the interests of Pacific island countries,” Mr. Jones said on the first day of the forum in Brisbane. He made the comment when asked about Chinese banks filling a vacuum in the Pacific. Meanwhile, Washington is stepping up efforts to support Pacific island countries in limiting Chinese influence. "We recognize the economic and strategic importance of the Pacific region, and we are committed to deepening engagement and cooperation with our allies and partners to enhance financial connectivity, investment and integration," said Brian Nelson, U.S. Treasury Undersecretary for Counterterrorism and Financial Intelligence. The United States is aware of the problem of Western banks de-risking in the Pacific region and is committed to addressing it, Nelson told the forum's participants. He said data showed that the number of correspondent banking relationships in the Pacific region has declined at twice the global average rate over the past decade, and the World Bank and the Asian Development Bank are developing plans to improve correspondent banking relationships. U.S. Treasury Secretary Janet Yellen said in a video address to the forum on Monday (July 8) that the United States is focused on supporting economic resilience in the Pacific region, including by strengthening access to correspondent banks. She said that when President Biden and Australian Prime Minister Anthony Albanese met at the White House last year, they particularly emphasized the importance of increasing economic connectivity, development and opportunities in the Pacific region, and a key to achieving that goal is to ensure that people and businesses in the region have access to the global financial system.